Crypto venture capitalists have brought the $2 trillion narrative to Wall Street.

Suddenly, the biggest story on Wall Street isn’t AI—it’s the explosive surge in near-delisted “junk” stocks experiencing reverse merger frenzies. In just a few short months, the U.S. capital markets have witnessed a record-breaking wave of increasingly sizable reverse mergers.

Public companies are shedding their traditional business lines and rebuilding around crypto reserves. Their stock prices are soaring—sometimes rising several or even dozens of times in a very short period. Wall Street has become a playground for large-scale crypto financial experiments. For the first time, crypto VCs have brought their stories directly to Wall Street’s front door.

DAT Fireworks: Crypto Point Men Take Over the U.S. Stock Market

When Primitive Ventures invested in Sharplink three months ago, the firm didn’t expect the U.S. crypto sector to crowd up so quickly. “Back then, hardly anyone was talking about these deals—today’s market buzz is completely different, and the transformation happened in just a month or two,” Primitive partner Yetta explained.

In June, Sharplink Gaming closed a $425 million funding round, becoming the first publicly traded Ethereum reserve company in the U.S. After the announcement, the company’s shares soared more than 10x at one point. Primitive, as the only Chinese-focused fund in the deal, became a hot topic in the crypto community.

“We found that crypto market liquidity was poor, but institutional buying power was exceptional. Bitcoin ETF volumes remained strong, and open interest in Bitcoin options on CME even surpassed Binance.” In April last year, Primitive internally reviewed its strategy and set a new investment direction—focusing on merging CeFi (centralized finance) and DeFi (decentralized finance). Today, they are among the busiest VCs in crypto.

Primitive now receives daily invitations from investment banks to participate in new crypto reserve deals. In this investment wave, i-banks serve as key intermediaries, organizing projects, sourcing and coordinating investors, and supporting project teams during investor roadshows.

In the last month, Primitive has spoken with more than 20 crypto reserve projects. So far, their only public crypto reserve investments are Sharplink and MEI Pharma, a Litecoin reserve company. This restraint comes from concerns about an overheated market. Since May, the team has closely monitored top-of-market signals.

“There’s no doubt that the bubble risk is much worse than a few months ago,” Yetta told Dongcha Beating. The team now publishes daily market reports and constantly evaluates exit strategies: “Crypto reserve companies are financial innovations. You can be long on the underlying assets over the long run, but in a downturn, there’s always severe deleveraging and bubble deflation risk.”

Pantera, by contrast, is going all in. The 12-year-old crypto VC even coined a new term for this sector—DAT (Digital Asset Treasury). In early July, Pantera launched the DAT Fund.

In their fundraising memo, Pantera partner Cosmo Jiang wrote: “As an investor, being at the origin of a new investment category is truly rare. Spotting this and acting quickly is key to unlocking early opportunities.”

Pantera’s pitch is simple: if a company’s Bitcoin Per Share is increasing year after year, owning its stock is like accumulating more and more Bitcoin over time.

Bitcoin reserve companies like MicroStrategy—and others that hold key cryptocurrencies—operate on the principle that when their market cap trades above the value of their crypto assets, they can use capital markets tools like private placements, convertibles, or preferred shares to raise funds and buy more crypto. Since the stock trades at a premium, the company can accumulate more assets at a lower cost.

Investors typically use the mNav indicator (Market Cap to Net Asset Value) to measure this premium and assess a company’s fundraising potential. “Of course the market moves up and down, and sometimes assets are overvalued. So raising capital through financial instruments is, in effect, selling volatility. That’s why the premium can persist,” Cosmo told Dongcha Beating.

In April, Pantera invested in DeFi Development Corps (DFDV), which holds Solana’s SOL tokens as reserves—making it the first U.S.-listed company to use a non-Bitcoin cryptocurrency as its reserve asset. Its shares have surged over 20x in the last six months.

This was a contrarian investment for Pantera; no one else wanted in early, so nearly all of DFDV’s $24 million raise came from Pantera.

DFDV’s team includes several former Kraken executives; the CFO also ran a Solana validator. Their deep expertise in both Solana and traditional finance was a decisive factor for Pantera. “We also built downside protections into the deal structure, but DFDV’s results far exceeded our expectations,” Cosmo said.

“I think the biggest catalyst was Coinbase getting into the S&P 500—suddenly, every fund manager in the world has to include crypto in their allocation.” Since Trump’s election, crypto has surged into mainstream capital markets: Circle’s IPO drew global attention to stablecoins, Robinhood’s RWA push made security tokenization hot, and now DAT has become the next growth concept.

Less than a month after the DFDV deal, Cantor Equity Partners came calling. DFDV’s success sped up SoftBank and Tether’s Bitcoin reserve plans, and CEP raised about $300 million from outside investors, with Pantera as lead.

Pantera’s investments in DFDV and CEP were funded from its flagship Venture Fund and Liquid Token Fund. The team initially thought these would be their only exposures in the sector.

But the sector’s momentum quickly exceeded expectations, and with investment limit constraints in those funds, Pantera launched a new dedicated fund.

Launched July 1, the DAT Fund targeted $100 million; by July 7, Pantera announced the raise was fully subscribed. Thanks to overwhelming LP demand, a second DAT Fund soon followed. By mid-month, the first DAT Fund was fully deployed.

In published deals, Pantera often serves as “Anchor”—the lead investor. DAT companies typically face initial liquidity challenges and discounts, so heavyweight backers step in to stabilize the market and price spread.

Playing Anchor Investor is also a deliberate Pantera strategy: “In the last two months, we’ve seen nearly 100 DAT deals. Pantera is usually the first call—because we’re early, are sector leaders, and have a reputation for writing large checks,” said Cosmo.

Pantera isn’t indiscriminate, either. They value DAT companies capable of “thought leadership” marketing. Investments in Sharplink and Bitmine were influenced by this. Bitmine was DAT Fund’s inaugural investment, with Pantera again serving as Anchor.

On June 2, Ethereum community leader Joseph Lubin led the reverse merger forming Sharplink, the first Ethereum reserve company. On June 12, Lubin and other core Ethereum figures published a fundamentals report via Etherealize for institutions.

On June 30, Bitmine emerged as the second Ethereum reserve company, with Wall Street crypto expert Thomas Lee going public with bullish calls on Ethereum—and appearing frequently in mainstream media. Around then, Sharplink’s stock took off and the “Ethereum arms race” became the hottest topic in the industry.

“To open true financial leverage, a DAT company’s market cap must reach at least $1-2 billion,” Cosmo told Dongcha Beating. “Only then can the company secure a real valuation premium and access institutional capital through convertibles or preferred equity.”

Before reaching that scale, DAT companies need to sell their story to ordinary investors—not just crypto insiders, but mainstream retail. “You have to get them to believe and participate. The market has to have conviction for the model to work.”

Building trust is critical for DAT companies. Traditional financial markets demand transparency and discipline, so teams must combine crypto-native skills with Wall Street-level professionalism, manage disclosures, and know SEC rules—essential for efficient, credible listings on U.S. exchanges.

“We do extensive due diligence—the static mNav figure isn’t what matters. What matters is clear management, reliable fundraising, and the capability to innovate new business models. That’s what makes a winning DAT founding team.”

Beyond Bitcoin, Ethereum, and Solana reserves, Pantera has invested in reserve companies for several major altcoins. The story for investors keeps evolving: for Bitcoin DATs, growth is purely financial engineering; for major tokens, returns come from staking and DeFi; for altcoin protocols, the underlying business generates real income, letting investors gain exposure via public equities.

Unlike Bitcoin and major token DATs, many altcoin DATs source initial reserves directly from protocol foundations or token investors.

For example, Hyperliquid’s reserve company Sonnet BioTherapeutics (SONN) received over 10 million HYPE tokens from Paradigm, a top crypto VC. Similarly, Ethena’s reserve company StablecoinX was set up by the Ethena Foundation, with PIPE investors allowed to invest with ENA or USDC.

With poor liquidity, altcoin DATs often see their stock prices soar after funding news—creating ample insider trading opportunities. In the SONN case, the July 14 announcement was preceded by a fourfold rally starting July 1.

BNB reserve company CEA, backed by YZi Labs, faced similar leaks. To prevent advance knowledge of the company name, the team pre-purchased several U.S. shell companies, randomly picking one at the last moment—yet front-running still happened hours before the official July 28 announcement.

Many investors worry altcoin DATs face “self-dealing” risks: with poor liquidity, it’s tough to unwind large holdings without taking a loss. Injecting the crypto asset into a DAT company turns illiquid tokens into tradable U.S. stock liquidity.

So, are DATs offering growth exposure or just facilitating exits? Investors need to distinguish carefully. “Many DATs play in regulatory gray areas, like listing on low-barrier boards. These short-term moves make it hard to establish stable disclosure and compliance frameworks. If there’s no real capital premium, it’s just musical chairs.”

Regulation is another risk. If the SEC classifies altcoins or on-chain assets as securities, DAT structures would require major overhauls. Yet Primitive and Pantera still see the U.S. market as superior: “Liquidity is better, listed investors have more protections, and DAT investments in the U.S. offer higher odds and returns than pure crypto bets,” Yetta said.

Beyond Wall Street: The Race for the Next ‘MicroStrategy’

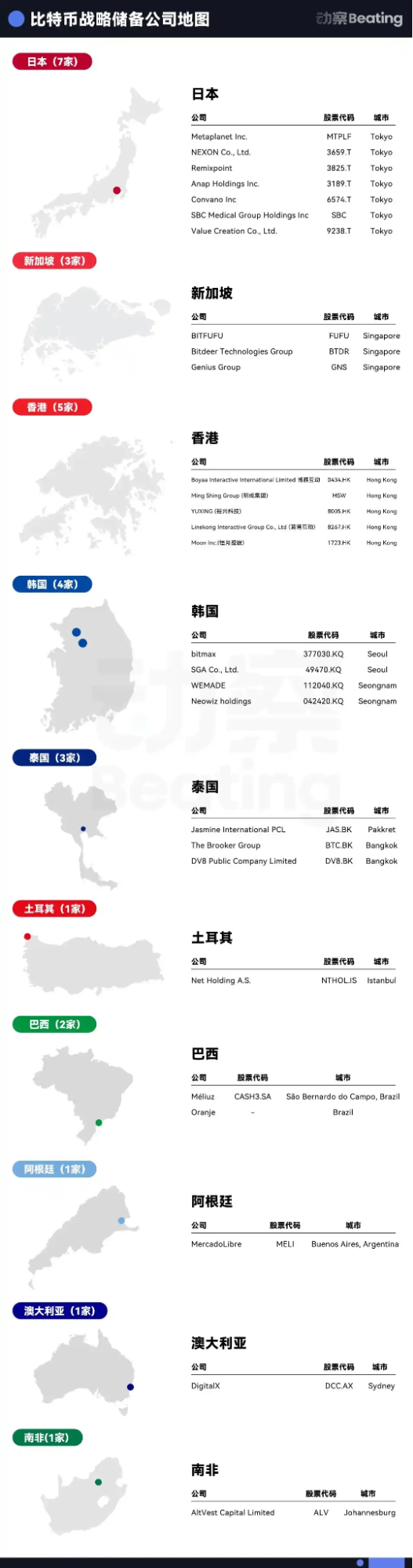

Wall Street’s reputation as the most efficient, inclusive, and liquid market is uncontested—if you want to repeat MicroStrategy’s success, Nasdaq is the place. But that doesn’t rule out opportunities in other markets. Outside of the U.S., everyone is racing to become the next Metaplanet.

Over the past year, Metaplanet’s stock premium has soared, delivering more than 10x returns. The “Asian miracle” blockbuster has shown investors new opportunities for regional arbitrage.

Asia’s markets are first movers in Bitcoin reserves. In mid-2023, ShuiDi Capital partnered with China Pacific Insurance Asset Management (Hong Kong) to launch the Pacific ShuiDi Fund, then took a stake in Boyaa Interactive, a Hong Kong-listed company beginning a Bitcoin buying plan. By 2024, MicroStrategy’s boom reaffirmed ShuiDi’s conviction. They now have stakes in five Hong Kong-listed companies with plans for at least ten by year-end.

“It’s obvious that U.S. Bitcoin and major token reserve companies are saturated. The next growth spurt will likely come from non-U.S. markets,” said Nachi—a crypto trader now investing in reserve companies. This year, he invested in Bitcoin reserve company Nakamoto Holdings and saw a 10x return almost immediately.

At the start of the year, Nachi became an LP in Mythos Venture, a fund dedicated to “Asian Bitcoin reserves.” Its latest investment: Thai-listed DV8, which raised 241 million baht, making it Southeast Asia’s first Bitcoin reserve company.

He also personally invested in other regional Bitcoin reserve deals, with most checks in the $1 million-plus range. In April, he participated in the acquisition of Oranje, Latin America’s first Bitcoin reserve company, which secured nearly $400 million in initial funding from Itaú BBA, Brazil’s largest commercial bank.

“Japan, Korea, India, Australia—they all have potential for this,” Nachi said. Since joining Mythos, he’s moved from LP to quasi-GP, reviewing deals. His focus is on identifying listed shell companies, a hot topic among Asian dealmakers.

“Being first” is the key to winning outside the U.S. It gives teams a head start and helps companies capture market attention. But it also turns the Bitcoin reserve story into a high-speed regional competition.

Shell company acquisition costs vary widely: some can be bought for $5 million, while the DV8 deal cost participants about $20 million.

From acquisition to trading, the typical timeline is 1 to 3 months, with regulatory approvals as the main bottleneck. But from opportunity discovery to deal close, it often takes at least six months or more.

The DV8 deal took nearly a year and closed in July. UTXO Management and Sora Venture—also the architects behind Metaplanet—led the investment.

Recently, Sora orchestrated the acquisition of Korea-listed software firm SGA. “Asian capital markets—especially in Southeast Asia—are pretty closed, but volumes are huge. Many foreign investors don’t get just how dynamic these spaces are,” Sora Ventures partner Luke told Dongcha Beating.

“Everyone’s racing against the clock, but in Asia, we have few real rivals,” Luke said. Local regulations are a major hurdle for overseas capital—most VCs lack acquisition and regulatory navigation experience in Asia.

Sora expedites deals by partnering with local contacts to navigate exchanges and regulators. For SGA, it took less than a month from initial talks to a signed transaction—a record for the Korean exchange.

Fundraising pace and strategy are additional challenges. “mNav only makes sense after significant Bitcoin accumulation—it’s a late-stage metric. Early on, companies use a different playbook from MicroStrategy.” Thanks to dual-class voting structures, U.S. DATs can dilute equity while retaining control.

Asian listed companies rarely have this, so dilution potential is limited. Teams have to carefully time fundraising and use core business cash flows to buy back shares for reverse dilution. DV8, for instance, has obtained the necessary licenses and will launch a crypto exchange soon.

Sora is wrapping up a Taiwan acquisition and working on a second Japanese Bitcoin reserve company. In May, it acquired 90% of Top Win, a U.S.-listed Hong Kong luxury distributor—which is about to rebrand as Asia Strategy. “Our goal is to build 9-10 ‘Metaplanet’ companies in Asia, roll them into a U.S.-listed parent, and give U.S. investors access to the Asia premium,” Luke said.

Top Win has been involved in acquisitions of Metaplanet, Hengyue Holdings, DV8, and SGA. Its first funding round is almost complete; Sora is using a “multi-investor, lower-ticket” approach, raising under $10 million with a six-month lock-up.

Luke hopes Top Win’s future capital stack will be 30% holdings in Asian companies and 60% in Bitcoin reserves—creating a differentiated narrative for investors. But it’s still mostly a thesis: whether the Asia premium is sustainable, or whether U.S. investors will buy it, remains to be proven by the market.

“Asia’s floor is high; its ceiling is low. For true scale, you have to be in the U.S.—that’s where global capital flows,” Luke said. No matter how many alpha narratives emerge abroad, everyone agrees the real beta comes from U.S. regulatory tailwinds.

“If the U.S. ever passes a national Bitcoin reserve bill, American government buying would set off copycat moves by governments and sovereign funds around the world. That could keep the price rising indefinitely,” said Nachi.

Rescue by 'Coin Stocks'

Compared with today’s stagnant crypto markets, the DAT sector is red hot—grabbing attention and providing a vital “exit” for crypto-focused capital. “Nearly every top-100 crypto project is considering spinning off a DAT company,” one investor told Dongcha Beating.

From late 2024 to early 2025, most crypto VC funds will reach maturity and begin new fundraising. But weak DPI metrics are scaring many LPs away, and many crypto funds have already wound down since the start of the year.

Since 2022, crypto venture valuations have ballooned; many projects collected eight-figure sums at seed, but few have delivered real innovation or tangible use cases. With the growth of crypto ETFs and FinTech/Crypto convergence, VCs remain LPs’ last way into the sector.

At the same time, shrinking liquidity is making exits harder. Retail isn’t buying “VC tokens” anymore, and listing fees are steep: “Top exchanges demand at least 5% of supply, so for a $100 million project, listing costs $5 million. Buying a U.S. shell company costs about the same.”

But the open U.S. regulatory climate is bringing fresh hope. Crypto reserve companies are now the best exit for large token holdings, and provide a new story to attract institutional money.

Beyond crypto VCs, midmarket investment banks are big winners. Bloomberg reports that 80% of midmarket broker time is now spent on DAT deals, and volume could triple by year-end.

The industry is racing to bring the entire $2 trillion crypto market onto Wall Street. In under two months, dozens of DAT companies have emerged.

Pantera expects the space to consolidate dramatically in three to five years: small DATs that can’t reach scale will face chronic discounts and get acquired cheaply by larger rivals. “DAT is a new treasury management laboratory—not a center for technical innovation. Ultimately, only two or three companies will survive.”

But for now, the music is just starting. Cosmo expects it will take at least another six months for the sector to reach full frenzy: “Nobody knows who will win. All we can do is back teams with a real shot at being among those two or three survivors.”

Disclaimer:

- This article is republished from [BlockBeats]. Copyright remains with the original author [BlockBeats]. If you have concerns about this republication, please contact the Gate Learn Team. The team will handle your issue according to its established procedures.

- Disclaimer: The views and opinions in this article are solely those of the author and do not constitute investment advice.

- Other language versions were translated by the Gate Learn Team. Except as noted, reproduction, distribution, or adaptation of this translation is prohibited unless Gate is explicitly referenced.

Related Articles

Solana Need L2s And Appchains?

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What Is Ethereum 2.0? Understanding The Merge